Home prices are continuing to deliver double-digit increases right now, so it’s understandable that many are concerned that we’re in a housing bubble like in 2006.

A closer look at current market data – and the following 3 illustrations – all indicate that history is in fact, not repeating itself.

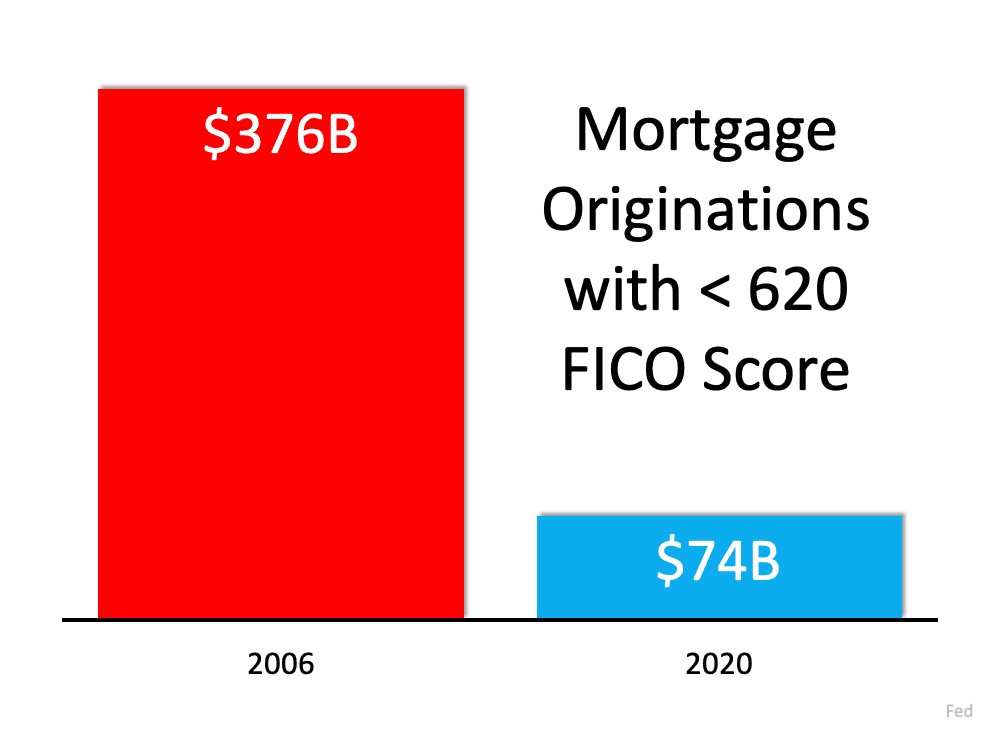

Today’s housing market is not driven by risky mortgage loans.

These figures are quite interesting, and their story begins with nearly everyone qualifying for a loan in 2006. The Mortgage Credit Availability Index (MCAI; from the Mortgage Bankers’ Association) indicates the availability of mortgage money; the higher the index, the easier money is obtained.

This index more than doubled from 2004 (378) to 2006 (869), with many mortgages granted to buyers with less than a 620 credit score. Notice the example that tells a different story today – MCAI stands at 130 and Chief Economists state that today’s loans equal no high-risk features and prudent mortgage underwriting.

Homeowners are not using their homes as ATMs this time.

When prices skyrocketed during the housing bubble, people refinanced their homes and pulled out large sums of cash. Prices began to fall, which caused many homeowners to spiral into a negative equity situation where their mortgage was higher than the value of the home.

Today, homeowners are letting their equity build. Tappable equity is the amount available for homeowners to access before hitting a maximum 80% combined loan-to-value ratio (thus still leaving them with at least 20% equity). In 2006, that number was $4.6 billion. Today, that number stands at over $8 billion.

Cash-out refinances (where the homeowner takes out at least 5% more than their original mortgage amount) is half of what is was in 2006 as illustrated below.

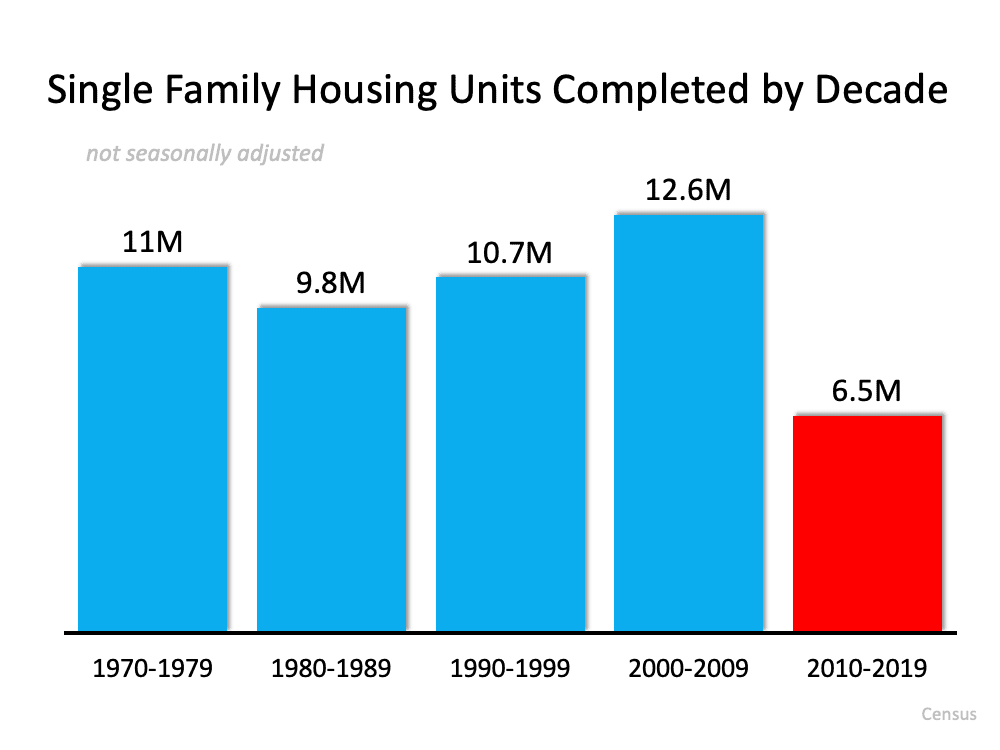

This time, it’s simply a matter of supply and demand.

Fear of missing out (FOMO) dominated the housing market leading up to the 2006 bubble, driving up buyer demand. The housing supply at that time was 7 months’ supply; today that number is barely 2 months.

Builders also overbuilt during that bubble but pulled back significantly over the next decade, and Chief Economists say it is that long-term decline in the construction of family homes is the major factor in the lack of available inventory today.

There are simply not enough homes to keep up with current demand, which is believed to be high especially because Millennials need houses.

While today’s market is not a repeat of 2006’s housing bubble, experts forecast that prices will keep rising for a while because inventory is so low.

Photograph and charts courtesy of Keeping Current Matters.